Central Banks Are Buying $2.4 Billion In Assets Every Hour As Their Balance Sheets Eclipse $20 Trillion Tyler Durden Fri, 05/22/2020 - 14:40

As Deutsche Bank's Peter Sidorov writes, "the global policy response to the rapidly unfolding coronavirus crisis has been substantial, in many ways unprecedented."

Just how unprecedented? One number highlighted by BofA's Michael Hartnett in his latest Flow Show report has the answer: in the past 8 weeks, central banks have been buying $2.4 billion per hour of financial assets.

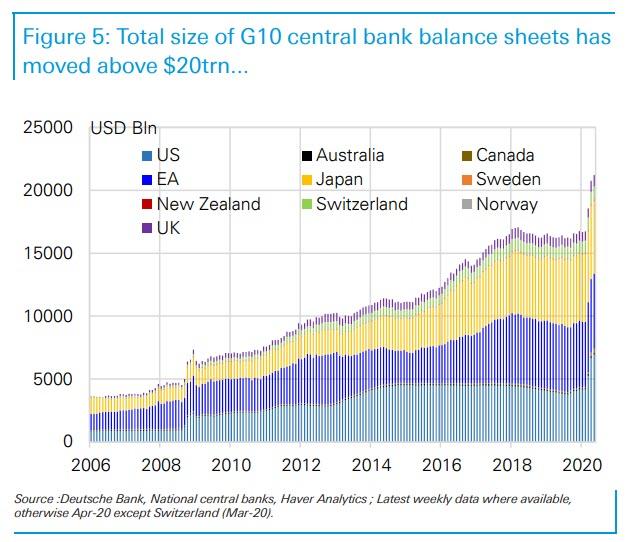

Here is another: as Deutsche Bank calculates, the combined G-10 central bank balance sheet is now above $20 trillion, catching up to its trendline since the financial crisis after stagnating around $16 trillion for the past two years...

... with the response to the coronavirus already double that observed after the global financial crisis.

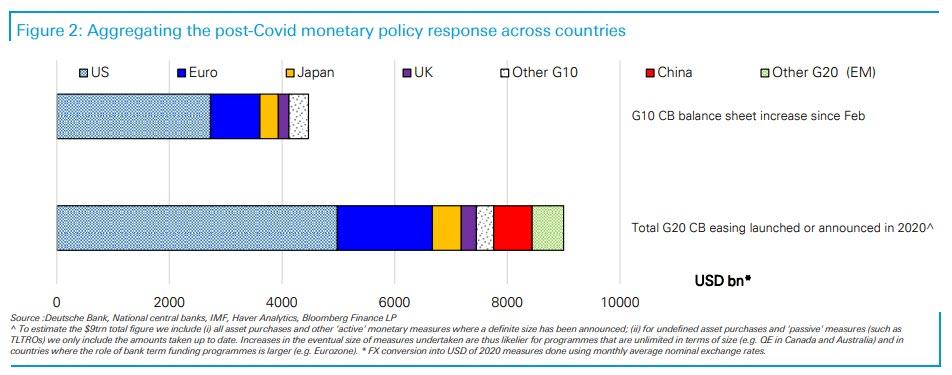

Some more details: central banks have undertaken or announced $9trn of measures since the start of the Covid crisis...

... with a $4.5trn increase in G10 central bank balance sheets since the end of February, bringing their total size to over $20trn.

As central banks continue to provide further support and with additional fiscal stimulus expected, this figure will likely move towards $20tn later this year, even if some of the announced measures are implemented in 2021 and beyond.

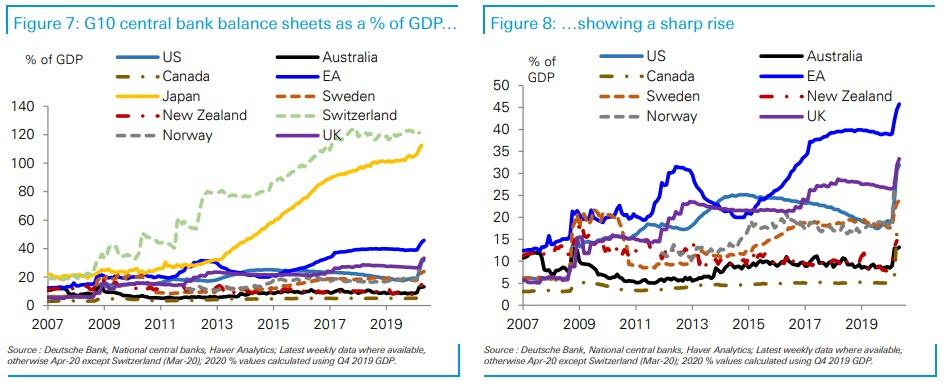

According to DB, the US has responded the most aggressively to date, with the amount of QE purchases implemented and new credit facilities announced accounting for around 55% of all measures across the G20 and 60% of the $4.5trn increase in G10 central bank balance sheets. This share will likely gradually ease over time as the Fed's aggressive pace of QE is easing while intervention in other countries, such as the newly discounted TLTRO3 in the euro area, are yet to come online. Relative to the size of the economy, the Fed and BoC have seen the largest increase in their balance sheets since the Covid shock — with a 12-13pp of GDP increases since the end of February, compared to rises of 6-7pp across the euro area, Japan and the UK.

When it comes to policy rates, across the DM universe rates were already cut towards the zero bound by the end of March and – with the exception of a 25bp Norges cut to 0.00% two weeks ago – have been unchanged since. The conversation has now moved onto whether more countries will join the Eurozone, Japan and Switzerland in negative-rates territory. Across EM, further room for rates easing remains in many countries, although the question of how low is too low is starting to come into view in some countries.

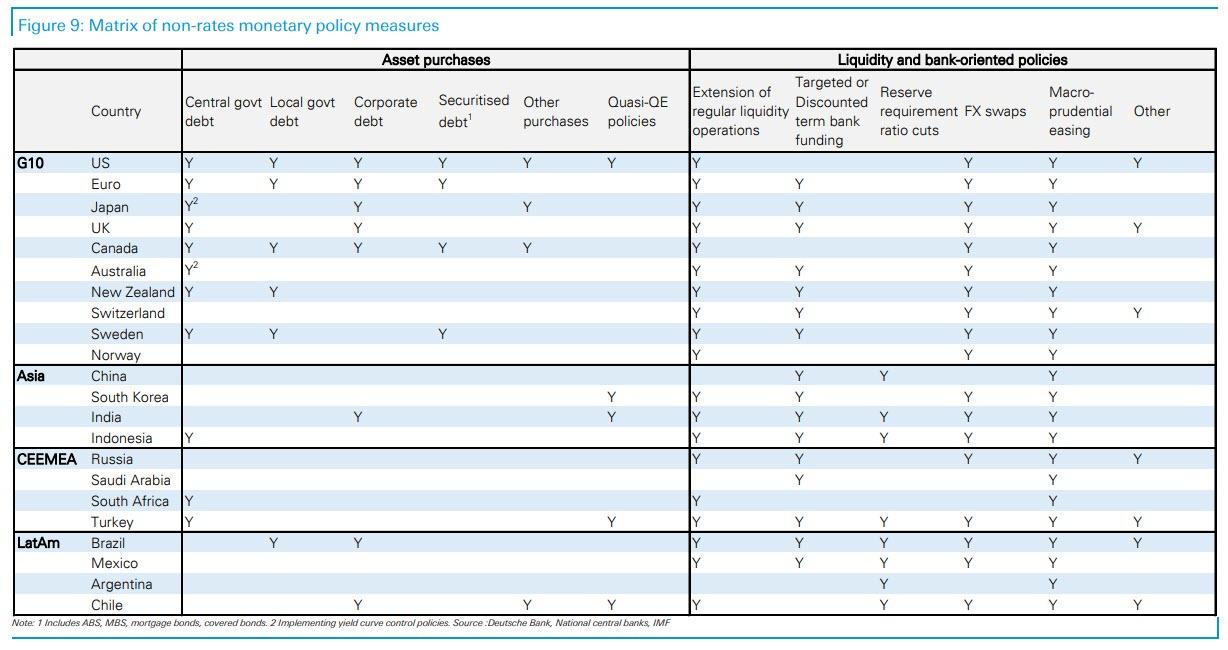

Finally, while all major countries have cut rates over the policy cycle, the non-standard measures that have been introduced vary widely across countries. As Sidorov notes, on asset purchases, most G10 economies and a few EM countries are now undertaking sovereign QE, although Australia has been the only country so far to join Japan in pursuing yield curve control. The introduction of purchases of local government and corporate debt and other assets has been more varied even among the DM economies, with the Fed seeing the broadest range of new measures, with its array of new credit-oriented facilities. On the banking side, macro-prudential easing and the expansion liquidity operations have been a global feature but the use of targeted or discounted term funding varies considerably across countries.

Below is a handy summary of non-rates monetary policy measures undertaken in the past two months:

via IFTTT

InoreaderURL: SECONDARY LINK