"Rental Policy Shock": 750,000 Households Are About To Be Evicted - What Happens To The Economy

With the Supreme Court officially striking down Biden's eviction moratorium and with most state-level restrictions set to expire over the next month, Goldman has calculated how sharply evictions could rise under current policy in order to estimate the potential impact on the economy.

First some big picture details:

-

Despite the severe recession, evictions actually declined during the coronacrisis due to the national eviction moratorium, with eviction filings declining 65% in Blue states and 61% nationwide.

-

Using rent delinquency data from real estate companies, the National Multifamily Housing Council, and the Census Pulse survey, the bank estimates that 2½-3½ million households are behind on rent, with $12-17bn owed to landlords.

-

Despite the $25bn dispersed from the Treasury to state and local governments, the process of providing these funds to households and landlords has been slow. Only 350k households received assistance in July, and at this pace, 1-2 million households will remain without aid and at risk of eviction when the last 2021 eviction bans expire on September 30.

Next, we jump right to Goldman's findings before digging deeper into the analysis. According to the bank:

-

The strength of the housing and rental market suggests landlords will try to evict tenants who are delinquent on rent unless they obtain federal assistance. And evictions could be particularly pronounced in cities hardest hit by the coronacrisis, since apartment markets are actually tighter in those cities.

-

Taken together, Goldman believes roughly 750k households will ultimately be evicted later this year under current policy.

-

Goldman expects that a small drag on consumption and job growth will result from an eviction episode of this magnitude, but the implications for covid infections and public health are probably more severe.

-

The end of the moratoriums would also exert downward pressure on shelter inflation as vacancy rates rise. Under our baseline estimates, post-moratorium evictions will raise the vacancy rate by about 1pp, which on its own would lower shelter inflation by 0.3pp in 2022, partially offsetting the intense upward pressure from the housing shortage.

With that in mind, we next look closer at the underlying causes behind the coming "Rental Policy Shock", as well as what comes next.

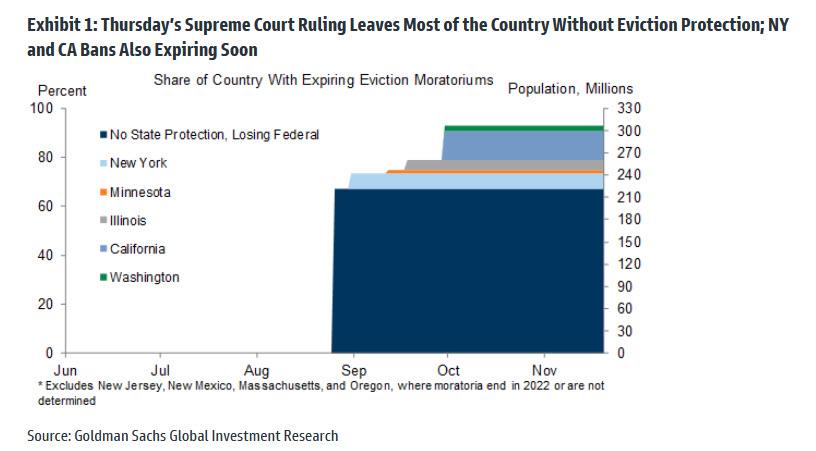

On Thursday, the Supreme Court overturned the federal eviction moratorium that had constrained the ability of landlords to evict tenants adversely affected by the pandemic recession. As shown in the chart below, because most states do not currently have eviction bans in place and because those that do are also set to expire by September, roughly 90% of the country will lose access to these emergency protections by the start of the fourth quarter.

The coming end of the eviction moratorium will result in a sharp and rapid increase in eviction rates in coming months unless Emergency Rental Assistance (ERA) funding is distributed at a much faster pace or Congress addresses the issue, for example in the upcoming reconciliation package. These key deadlines are summarized in the table below.

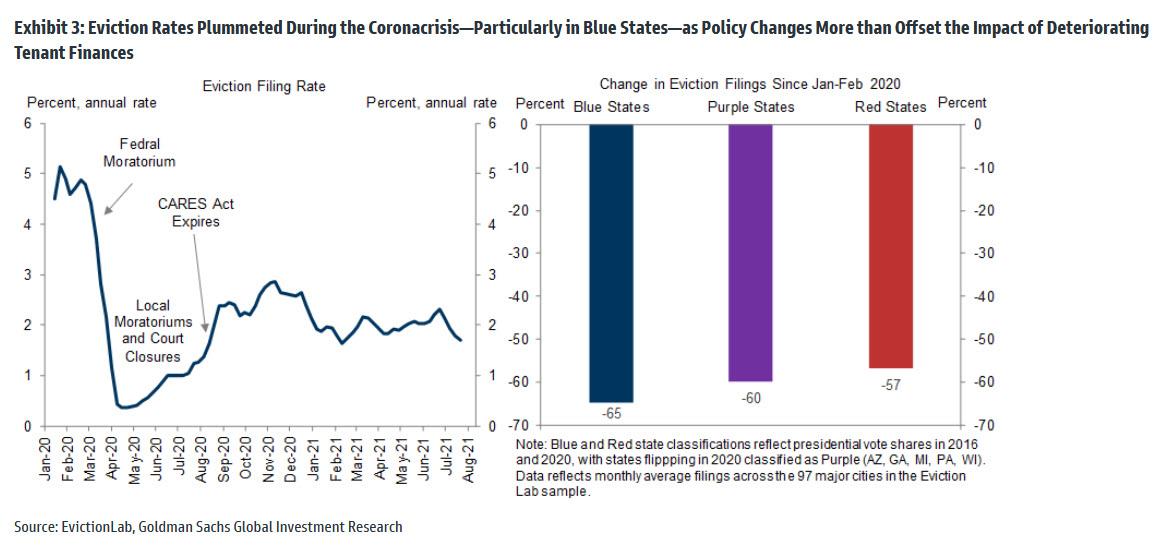

The tenant protection policies listed above significantly reduced evictions during the first 18 months of the pandemic, with eviction rates actually falling instead of rising as typically happens during a recession. Because of the legal gray area and income-eligibility requirements of the federal eviction bans, state and local moratoriums have often been more effective in preventing evictions. As shown in the left panel of the next chart, eviction rates plummeted to near-zero while the strictest eviction bans of spring 2020 were in effect, and on average, eviction filing rates remain less than half their pre-crisis pace.

The right panel above shows that eviction filings have generally fallen more dramatically in liberal states and cities adopting more stringent protections like California and New York (-65% across Blue States). These states are also more likely to interpret the federal moratoriums more generously than Red States.

Economic Impact of the Moratoriums

The eviction moratoriums primarily affected the real economy through their impact on tenant-occupied housing consumption and consumer cash flows, both of which were highly positive: the housing consumption category continued to rise during the crisis in spite of the surge in unemployment (+0.9% in 2020 and +0.8% in 1H21, real basis). However, the category represents only 2.5% of GDP, so the direct impact on GDP levels through this channel was probably small (0.1-0.2% of GDP).

Eviction Backlog

Obviously, the eviction moratorium had extremely favorable consequences for the economy - after all it delayed the realization of true supply and demand at the expense of taxpayers and massive debt monetization. However, this period of involuntary taxpayer generosity is coming to an end and as of this moment, estimates of rental delinquencies run the gamut from under 1mn units to upwards of 15mn, with the wide range reflecting the rapid changes in the labor and rental markets over the last year, as well as the lack of timely and representative data on the subject. Goldman's estimates, shown below, indicate 1-2mn households at risk of eviction even after next month’s federal aid distributions, of which roughly 750k households would be evicted under the status quo.

As shown in the exhibit above, Goldman estimates that the number of housing units at risk of eviction, based on uncollected tenant revenues in 2021Q2 for large property managers, representing 20mn tenant-occupied housing units, and based on survey data reporting the share of consumers who owe back rent and also “lost employment income” during the pandemic, representing the remaining 25mn units. Because the moratoriums also deferred hundreds of thousands of evictions unrelated to the pandemic, one should also add an additional backlog to reflect these missing filings.

Together, the bank estimates that 2½-3½ million households are significantly behind on rent and at risk of eviction without policy support. Since roughly half of eviction filings historically result in eviction (47% over 2006-2016), Goldman assumes that barring a new eviction ban from Congress or a much faster pace of ERA distribution, 750k households will face eviction in the fall and winter months. With 8-9 million Americans currently unemployed and emergency unemployment programs winding down, the sudden loss of tenant protections could plausibly generate an eviction episode of this magnitude.

Translating these figures to a dollar amount of back rent based on the stock and flow of bad tenant debt among residential REITs, implies 4.4 months of rent payments outstanding on average across tenants who are behind on rent. This is consistent with research from the Center for Budget and Policy Priorities estimating average tenant debt at 3 months’ rent. Taken together, some $12-17 billion of bad tenant debt accumulated during the crisis.

Yet Another Bottleneck

With $25bn already dispersed from the Treasury to state and local governments and another $20bn available, the size of the Congressional allocation would appear more than sufficient to prevent an eviction crisis. But so far, the process of recovering back rents has been disappointingly slow, in part because doing so requires a significant amount of matching of information from the renter and the landlord. After doubling month-over-month in June to $1.5bn, the pace of distributions plateaued at $1.7bn in July (and $4.5bn cumulatively). Because of this and because utilities and electric bills are absorbing a significant minority of these funds, under current policy, a significant share of the 2½-3½ million households behind on rent could ultimately face eviction later this year.

As shown in Exhibit 6, at the current monthly processing pace of 350k households, 1-2 million delinquent households would remain without ERA aid at the start of Q4 when the last 2021 eviction bans are set to expire (NY, WA).

At the same time, the strength of the housing and rental market suggests landlords will try to evict delinquent units unless they can obtain federal funding. In fact, as shown in the next chart, apartment markets are actually tighter in cities hardest hit by the coronacrisis. This reduces the incentive for landlords to negotiate with delinquent tenants or wait for federal aid.

Economic Consequences

The final question is what would the coming surge in evictions mean for employment, consumption, and inflation?

Here Goldman's economists write that eviction increases the likelihood of a subsequent unemployment spell by around 2%. Based on 750k units and 1.17 payroll jobs per household, Goldman estimates 20k incremental job losses over the next year as a result of the end of the moratoriums (naturally, that number is far too low).

While the consumption effects of such job losses would be small for economy as a whole, the end of the moratoriums also means that households who skipped rent payments would need to cut back in other areas. Based on a marginal propensity to consume of 0.7 for delinquent units during Q2, Goldman estimates a ¼% drag on Q4 consumption growth from this channel.

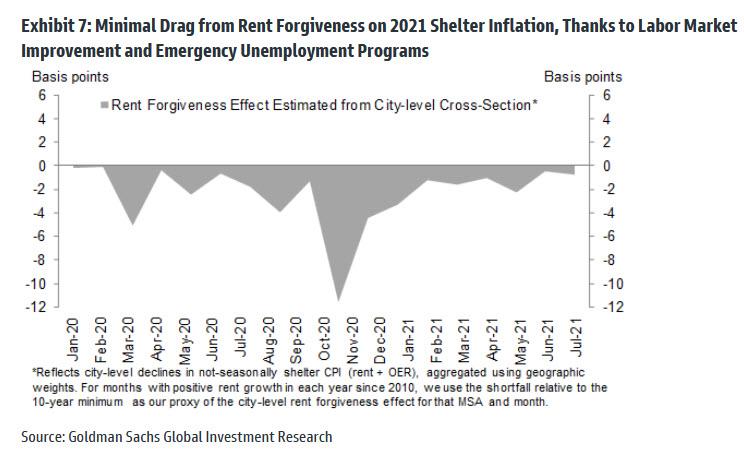

We conclude by analyzing the inflation implications of these developments. While small in GDP terms, housing rental prices provide the source data for 17% of the core PCE inflation basket and 40% of the core CPI basket. Here Goldman writes that in its view, eviction moratoriums reduced shelter inflation early in the crisis by increasing the prevalence of rent forgiveness: the CPI statisticians impute a 95% price reduction for such housing units. Updating its previous proxy based on city-level rent declines, Goldman estimates rent forgiveness lowered PCE shelter prices by 0.32% during 2020 and by another 0.1% in 2021.

There is a silver lining: a surge in evictions should create new inventory of available rental housing, partially offsetting rapidly rising housing costs,.

So looking ahead, the end of the moratoriums will likely boost the market supply of rental units, because evicted tenants often move in with family members or leave the urban rental market entirely. Based on the historical relationship between vacancies and shelter inflation (holding unemployment constant), a 500k rise in vacancies would boost the rental vacancy rate by 1pp and exert 0.3pp of downward pressure on shelter inflation in 2022.

Despite this "benefit", based on the continued improvement in the labor market, robust housing market fundamentals, and the sharp pickup in mid-year rental prices, Goldman still forecast PCE housing inflation to pick up from 2.2% currently to 3.5% at year-end and 4.6% in 2022. That means that housing is about to become completely unaffordably to virtually anyone outside of the top 1%. As for the original American Dream (i.e. owning a house), of all those who are about to get evicted, our advice: aim lower...

via IFTTT

InoreaderURL: SECONDARY LINK